SCDL Solved Assignments on Strategic Finance Notes

Strategic Finance Notes SCDL Sample Papers

Strategic Finance Notes SCDL Sample Papers

Q.3 With the help of models explain inventory control for working capital management.

Ans INVENTORY MANAGEMENT

Introduction: Inventories are stock of the product a company is manufacturing for sale and components that make up the product.

Nature of Inventories: The various forms in which inventories exists in manufacturing company are

· Raw Materials: are basic inputs that are converted into finished product through the manufacturing process.

· Work-in-Progress: inventories are semi-manufactured products.

· Finished Goods: inventories are those completely manufactured products, which are ready for sale.

Need to hold Inventories:

· Transactions motive: emphasizes the need to maintain inventories to facilitate smooth production & sales operation.

· Precautionary motive: necessitates holding of inventories to guard against the risk of unpredictable changes in demand & supply forces & other factors.

· Speculative motive; influences the decision to increase or reduce inventory levels to take advantage of price fluctuations.

Objective of Inventory Management

· To maintain a large size of inventory for efficient and smooth production & sales operations.

· To maintain a minimum investment in inventories to maximise profitability.

The firm should always avoid a situation of over investment or under investment in inventories.

The major dangers of over investment are:

a) Unnecessary tie up of the firm’s funds and loss of profit,

b) Excessive carrying costs,

c) Risk of liquidity.

The major dangers of under investments are:

a) Production hold-ups.

b) Failure to meet delivery commitments.

An effective inventory management should:

· Ensure a continuous supply of raw materials to facilitate uninterrupted production.

· Maintain sufficient stocks of raw materials in periods of short supply and anticipate price changes,

· Maintain sufficient finished goods inventory for smooth sales operation, and efficient customer service,

· Minimize the carrying cost and time, and

· Control investment in inventories and keep it at an optimum level.

Q.4. With the help of models explain cash control for working capital management.

Ans CASH MANGEMENT

Cash is the most important current asset in any business operations. The term cash includes coins, currency and cheques held by the firm, and balances in its bank account.

Cash management is concerned with managing of

1. cash flow into and out of the firm

2. cash flows within the firm

3. cash balances held by the firm by financing deficit or investments of surplus cash

All these activities are to be done at minimum cost.

Facets of Cash management:

Cash planning:

Cash inflows and outflows should be planned to project cash surplus or deficit for each period of planning period. Cash budget is prepared for this purpose.

Managing cash flows:

Cash flow should be properly managed. Inflow of cash should accelerate while outflow should decelerate as far as possible.

Optimum cash level:

The firm should determine optimum cash level considering the cost of excess cash and danger of cash deficiency.

Investing surplus cash:

Surplus cash should be properly invested in short term opportunities like deposits, corporate lending, marketable securities to earn profits.

Motives of Holding Cash

Transaction motive

The transaction motive requires a firm to hold cash to conduct its business in ordinary course to make payments for purchases, wages, other operating expenses, taxes etc. Transaction motive mainly refers to holding cash to meet anticipated payments whose timing is not perfectly matched with cash receipts.

Precautionary motive

It is needed to hold cash for contingencies in future. It gives cushion to withstand the unexpected emergency. Less cash is required to be maintained for emergency if cash flows are fairly accurate. The precautionary balance is kept in cash form or marketable securities.

Speculative motive

It is holding cash for investing it in profit making opportunities as and when they arise.

Cash forecasting.

Short-term forecasting.

Short-term forecasting is done for the following reasons.

To determine operating cash requirements.

To anticipate short-term financing: which is generally obtained from bank.

To manage investment of surplus cash : which help managers to study the market and invest in better yield investments.

Short-term forecasting methods

1. Receipts and disbursement method

This sources of cash inflow like operating, non operating and financial inflows etc. are considered on receipt side. Whereas on disbursement side cash outflows like operating expenses, capital expenditure, contractual payments, taxes and likes are considered to come to work out cash requirements.

Receipt and disbursement method is sound tool as it gives clear picture of all items.

2. Adjusted net income method

This method involves tracing of working capital flows. Its objectives are to project company’s need for cash at a future date and to show whether the company can generate it internally or borrow from market.

Long term cash forecasting:

It is generally for the period of 3 to 5 years. It is not as detail as short term forecast.

It helps company to find future financial needs and improves corporate planning.

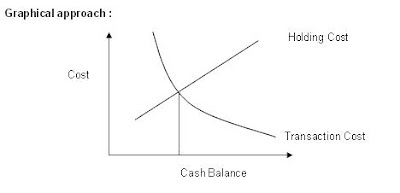

Determining the optimum cash balance:

Organisation should keep enough liquidity so that operations do not suffer and should not loose profit due to high liquidity. Then how one should decide on optimum cash balance? There are two situations, which are explained below.

Optimum Cash balance

Q.7 What are the reasons for restructuring through share buybacks? Explain Indian context and regulations.

Ans. The provisions regulating buy back of shares are contained in Section 77A, 77AA and 77B of the Companies Act,1956. These were inserted by the Companies (Amendment) Act,1999. The Securities and Exchange Board of India (SEBI) framed the SEBI(Buy Back of Securities) Regulations,1998 and the Department of Company Affairs framed the Private Limited Company and Unlisted Public company (Buy Back of Securities) Regulations,1998 pursuant to Section 77A(2)(f) and (g) respectively.

Objectives of Buy Back:

Shares may be bought back by the company on account of one or more of the following reasons

i. To increase promoters holdingii. Increase earning per shareiii. Rationalize the capital structure by writing off capital not represented by available assets. iv. Support share valuev. To thwart takeover bidvi. To pay surplus cash not required by business

Infact the best strategy to maintain the share price in a bear run is to buy back the shares from the open market at a premium over the prevailing market price.

Resources of Buy Back

A Company can purchase its own shares from

(i) free reserves; Where a company purchases its own shares out of free reserves, then a sum equal to the nominal value of the share so purchased shall be transferred to the capital redemption reserve and details of such transfer shall be disclosed in the balance-sheet or

(ii) securities premium account; or

(iii) proceeds of any shares or other specified securities. A Company cannot buyback its shares or other specified securities out of the proceeds of an earlier issue of the same kind of shares or specified securities.

Conditions of Buy Back

(a) The buy-back is authorised by the Articles of association of the Company;

(b) A special resolution has been passed in the general meeting of the company authorising the buy-back. In the case of a listed company, this approval is required by means of a postal ballot. Also, the shares for buy back should be free from lock in period/non transferability.The buy back can be made by a Board resolution If the quantity of buyback is or less than ten percent of the paid up capital and free reserves;

(c) The buy-back is of less than twenty-five per cent of the total paid-up capital and fee reserves of the company and that the buy-back of equity shares in any financial year shall not exceed twenty-five per cent of its total paid-up equity capital in that financial year;

(d) The ratio of the debt owed by the company is not more than twice the capital and its free reserves after such buy-back;

(e) There has been no default in any of the followingi. in repayment of deposit or interest payable thereon,ii. redemption of debentures, or preference shares oriii. payment of dividend, if declared, to all shareholders within the stipulated time of 30 days from the date of declaration of dividend or iv. repayment of any term loan or interest payable thereon to any financial institution or bank;

(f) There has been no default in complying with the provisions of filing of Annual Return, Payment of Dividend, and form and contents of Annual Accounts;

(g) All the shares or other specified securities for buy-back are fully paid-up;

(h) The buy-back of the shares or other specified securities listed on any recognised stock exchange shall be in accordance with the regulations made by the Securities and Exchange Board of India in this behalf; and

(i) The buy-back in respect of shares or other specified securities of private and closely held companies is in accordance with the guidelines as may be prescribed.

Disclosures in the explanatory statement

The notice of the meeting at which special resolution is proposed to be passed shall be accompanied by an explanatory statement stating - (a) a full and complete disclosure of all material facts; (b) the necessity for the buy-back; (c) the class of security intended to be purchased under the buy-back; (d) the amount to be invested under the buy-back; and (e) the time-limit for completion of buy-back

Sources from where the shares will be purchased

The securities can be bought back from

(a) existing security-holders on a proportionate basis;Buyback of shares may be made by a tender offer through a letter of offer from the holders of shares of the company or

(b) the open market through(i). book building process;(ii) stock exchanges or

(c) odd lots, that is to say, where the lot of securities of a public company, whose shares are listed on a recognized stock exchange, is smaller than such marketable lot, as may be specified by the stock exchange; or

(d) purchasing the securities issued to employees of the company pursuant to a scheme of stock option or sweat equity.

Filing of Declaration of solvency

After the passing of resolution but before making buy-back, file with the Registrar and the Securities and Exchange Board of India a declaration of solvency in form 4A. The declaration must be verified by an affidavit to the effect that the Board has made a full inquiry into the affairs of the company as a result of which they have formed an opinion that it is capable of meeting its liabilities and will not be rendered insolvent within a period of one year of the date of declaration adopted by the Board, and signed by at least two directors of the company, one of whom shall be the managing director, if any: No declaration of solvency shall be filed with the Securities and Exchange Board of India by a company whose shares are not listed on any recognized stock exchange.

Register of securities bought back

After completion of buyback, a company shall maintain a register of the securities/shares so bought and enter therein the following particularsa. the consideration paid for the securities bought-back,b. the date of cancellation of securities,c. the date of extinguishing and physically destroying of securities and d. such other particulars as may be prescribed

Where a company buys-back its own securities, it shall extinguish and physically destroy the securities so bought-back within seven days of the last date of completion of buy-back.

Issue of further shares after Buy back

Every buy-back shall be completed within twelve months from the date of passing the special resolution or Board resolution as the case may be.

A company which has bought back any security cannot make any issue of the same kind of securities in any manner whether by way of public issue, rights issue up to six months from the date of completion of buy back.

Filing of return with the Regulator

A Company shall, after the completion of the buy-back file with the Registrar and the Securities and Exchange Board of India, a return in form 4 C containing such particulars relating to the buy-back within thirty days of such completion. No return shall be filed with the Securities and Exchange Board of India by an unlisted company.

Prohibition of Buy Back

A company shall not directly or indirectly purchase its own shares or other specified securities - (a) through any subsidiary company including its own subsidiary companies; or (b) through any investment company or group of investment companies; or

Procedure for buy back

a) Where a company proposes to buy back its shares, it shall, after passing of the special/Board resolution make a public announcement at least one English National Daily, one Hindi National daily and Regional Language Daily at the place where the registered office of the company is situated.

b) The public announcement shall specify a date, which shall be "specified date" for the purpose of determining the names of shareholders to whom the letter of offer has to be sent.

c) A public notice shall be given containing disclosures as specified in Schedule I of the SEBI regulations.

d) A draft letter of offer shall be filed with SEBI through a merchant Banker. The letter of offer shall then be dispatched to the members of the company.

e) A copy of the Board resolution authorising the buy back shall be filed with the SEBI and stock exchanges.

f) The date of opening of the offer shall not be earlier than seven days or later than 30 days after the specified date

g) The buy back offer shall remain open for a period of not less than 15 days and not more than 30 days.

h) A company opting for buy back through the public offer or tender offer shall open an escrow Account.

Penalty

If a company makes default in complying with the provisions the company or any officer of the company who is in default shall be punishable with imprisonment for a term which may extend to two years, or with fine which may extend to fifty thousand rupees, or with both. The offences are, of course compoundable under Section 621A of the Companies Act,1956.